How to Choose the Right Life Insurance Policy: Term vs Whole Life Explained

Life insurance isn’t something most people enjoy thinking about. But once you have a family, a mortgage, or anyone who depends on your income, it stops being optional and starts becoming part of responsible financial planning.The real confusion usually comes down to one question: **term life insurance or whole life insurance?**The answer isn’t universal. It depends on your income, long-term goals, debt, and how you want your money to work over time.Let’s break it down clearly.

What Is Term Life Insurance?

Term life insurance provides coverage for a specific period — typically 10, 20, or 30 years.If you pass away during that term, your beneficiaries receive a tax-free death benefit.If you outlive the term, the policy expires.

Why Term Life Insurance Is Popular

• Lower monthly premiums

• Simple structure

• High coverage amounts for lower cost

• Ideal for income replacement

This is often the best choice for young families. You can secure a large death benefit — $500,000 or even $1 million — for surprisingly affordable premiums.

When Term Makes Sense

Term life insurance works best if:

• You want protection during your working years

• You have a mortgage or young children

• You’re focused on budget efficiency

• You invest separately for retirement

It’s straightforward. Protection only. No built-in savings component.

What Is Whole Life Insurance?

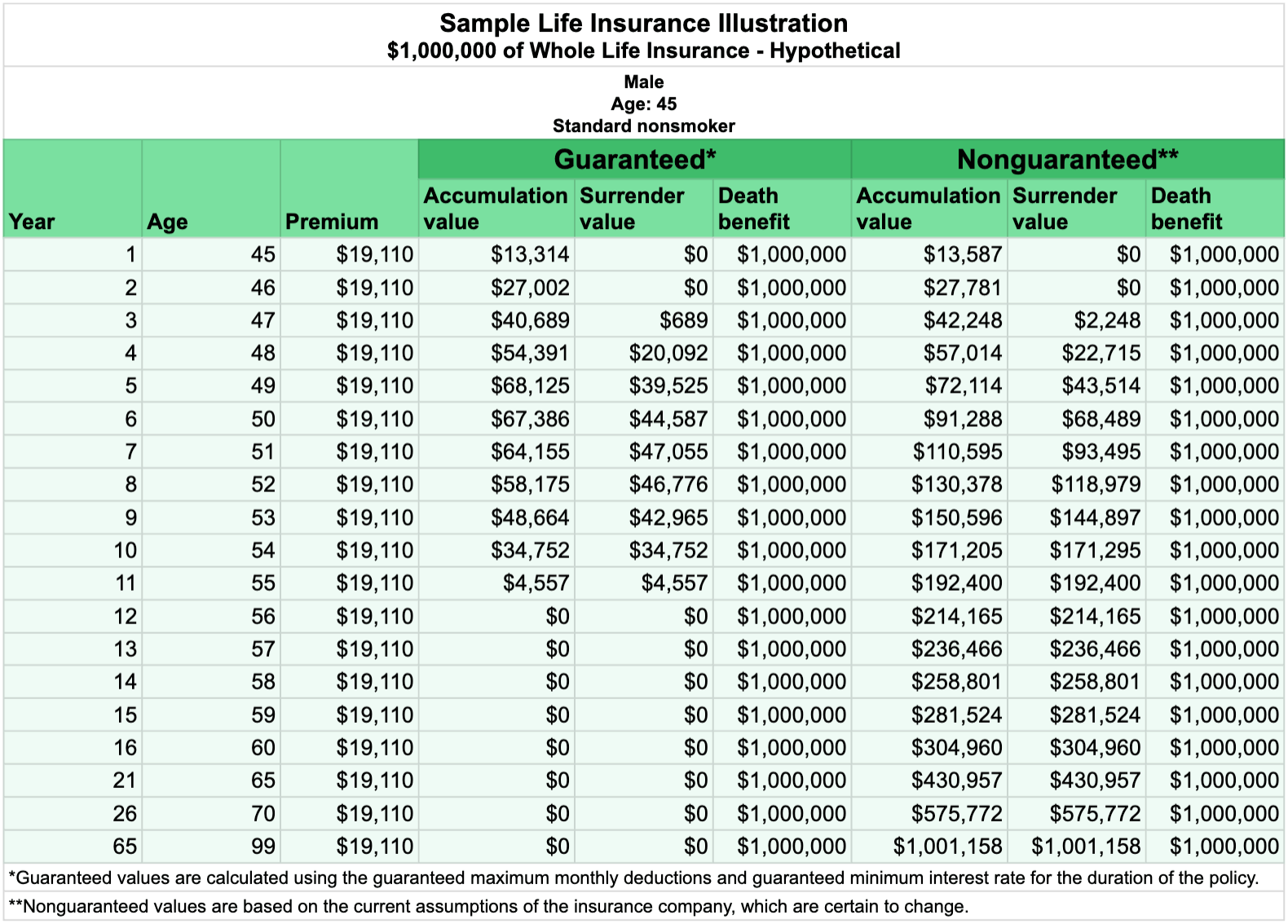

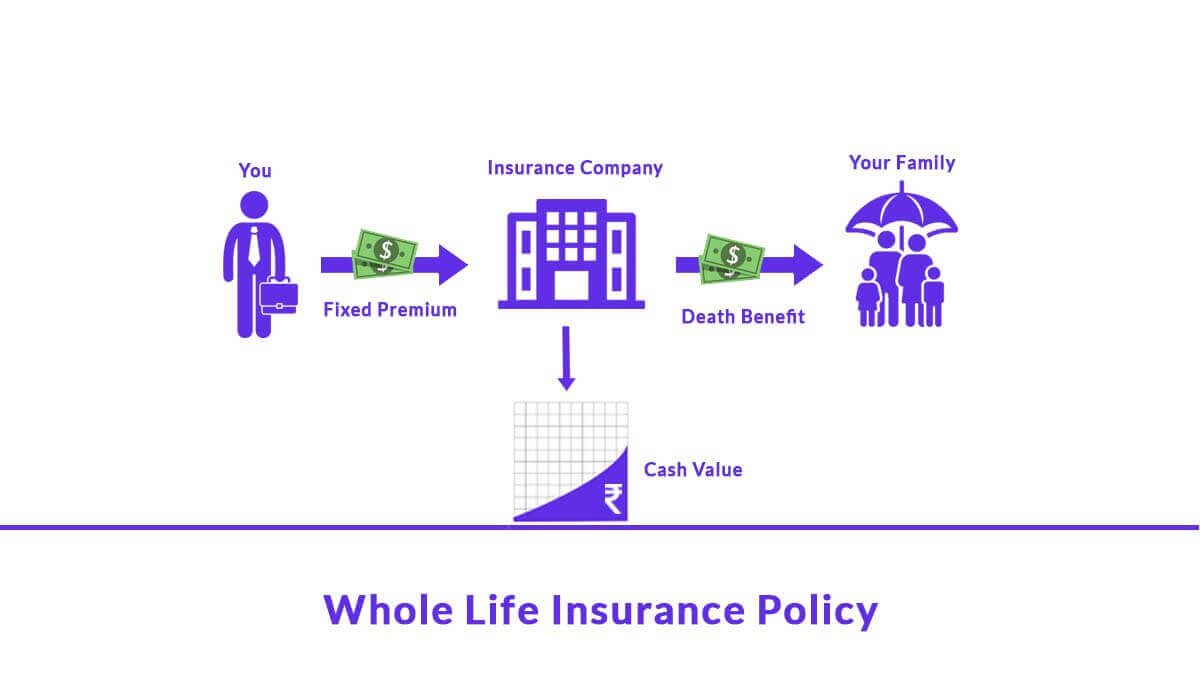

Whole life insurance is permanent coverage. It doesn’t expire as long as premiums are paid.It also builds cash value, which grows over time and can be borrowed against.

Key Features of Whole Life Insurance

• Lifetime coverage

• Fixed premiums

• Guaranteed death benefit

• Cash value accumulation

Part of your premium goes toward the insurance cost. The rest builds a tax-advantaged savings component inside the policy.

When Whole Life Makes Sense

Whole life may fit if:

• You want lifelong coverage

• You’ve maxed out retirement accounts

• You’re focused on estate planning

• You prefer guaranteed growth over market volatility

It’s often used in high-income financial planning strategies or legacy planning.

Term vs Whole Life: Side-by-Side Comparison

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Length | 10–30 years | Lifetime |

| Premium Cost | Lower | Higher |

| Cash Value | No | Yes |

| Investment Component | None | Guaranteed growth |

| Best For | Income protection | Long-term wealth strategy |

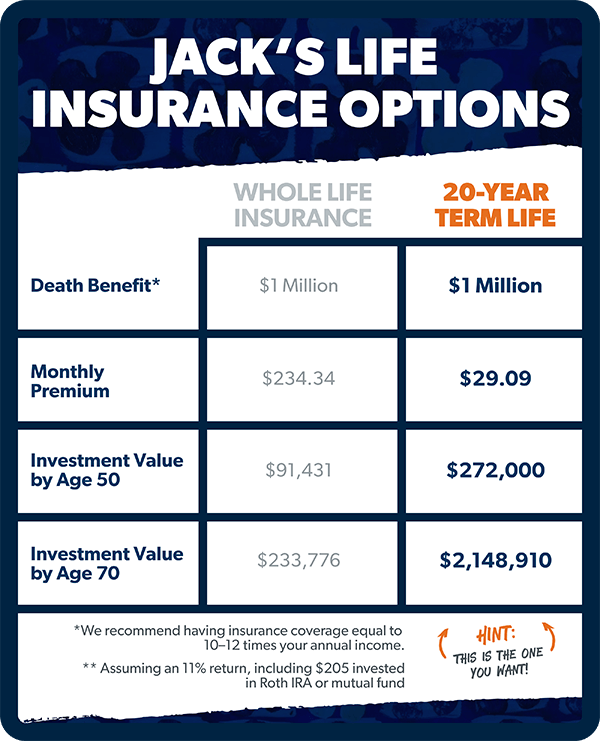

| The premium difference can be dramatic. A healthy 30-year-old might pay $30–$50 per month for term coverage but several hundred dollars monthly for whole life. |

Cost Comparison Example

Let’s say you’re 35 years old and want $500,000 in coverage:

• Term life (20-year policy): Often $25–$45/month

• Whole life: Often $300–$600/month

That gap matters. The question becomes whether the added cost aligns with your financial goals.

How to Decide Which Policy Is Right for You

There’s no one-size-fits-all answer. But a few principles make the decision easier.

1. Define the Purpose of the Policy

If your main goal is income replacement while your kids are young, term life insurance is usually the most efficient choice.If your goal includes estate preservation or tax-advantaged cash growth, whole life insurance becomes more relevant.

2. Evaluate Your Budget

Insurance should protect your finances — not strain them. Overcommitting to high whole life premiums can limit your ability to invest elsewhere.

3. Consider Your Investment Strategy

Many financial advisors suggest “buy term and invest the difference.”The idea is simple: choose affordable term coverage and invest the money you save in retirement accounts or brokerage accounts.Over decades, disciplined investing can outperform the guaranteed growth inside whole life policies.

4. Think Long Term

Will you still need coverage after 20–30 years?If you build enough assets to self-insure, term coverage may be all you need.If you want permanent coverage regardless of future wealth, whole life offers certainty.

Hybrid Option: Convertible Term Policies

Some term policies allow conversion to whole life without a medical exam.This provides flexibility. You can start affordable and shift later if your strategy changes.

Common Mistakes to Avoid

• Buying too little coverage

• Waiting too long to apply

• Choosing based solely on price

• Not comparing multiple quotes

Rates vary widely by insurer, age, health, and lifestyle. Shopping around matters.

FAQ: Term vs Whole Life Insurance

Is term life insurance better than whole life?

For most families focused on income protection and affordability, term life insurance provides the best value. Whole life serves more complex, long-term financial strategies.

Can I convert term life to whole life?

Many policies allow conversion during a set period without additional underwriting. Check policy details before purchasing.

Does whole life insurance build cash value quickly?

Cash value typically grows slowly in early years due to fees and commission structures. It becomes more meaningful over time.

How much life insurance coverage do I need?

A common guideline is 10–15 times your annual income, but debt, future expenses, and dependents should shape the final number.

Final Thoughts

Choosing between term life insurance and whole life insurance isn’t about which product is “better.” It’s about alignment.Term life insurance is efficient, affordable, and powerful for protecting income during critical years.Whole life insurance offers permanence and structured cash value growth for those who need it.Clarity comes from understanding your financial stage, responsibilities, and long-term vision. The right policy should give you peace of mind — not financial pressure.